BRIEF FROM THE CEMENT ASSOCIATION OF CANADA

Executive Summary

Cement is a strategic commodity and a critical component of our nation’s infrastructure. Cement underpins the construction industry – as the key ingredient in concrete – and there is little built without concrete. In fact, concrete is the most used man made commodity in the world.

Furthermore, cement and concrete play an important role in making Canada’s infrastructure greener and therefore sustainable, as well as being extremely energy efficient products that are used in projects ranging from concrete highways, green buildings, water and sewer installation and countless others. So when we seek to explore ways to achieve a sustained economic recovery in Canada, and how to create quality sustainable jobs, there is no question that sustainable infrastructure investments are a significant part of the solution.

Recently, the Canadian economy experienced one of the worst economic downturn in many years. Given the right mix of economic policies, the Canadian government helped to sail our economy through the storm better than almost all other nations. One of the economic keys to success involved the investment of billions of dollars in physical infrastructure which helped keep Canadians employed and aided Canadian productivity.

Even though the economy has been slowly recovering, like most others, our industry has been significantly impacted by the global economic recession, with reduced demand for cement and concrete across Canada and in the U.S., which is our primary export market. For the first time in decades, our industry has experienced layoffs and prolonged shut-downs, both of which affect Canadians from Coast to Coast to Coast and the ability to complete infrastructure projects efficiently and cost-effectively. However, significant threats remain on the horizon, including a return to recession in the U.S., and a sustained high value of the Canadian dollar which is impacting our export market.

Recommendation #1: The government should make improvements in the long-term benefits of infrastructure investments by ensuring sustainability concepts are included in project design, such as the choice of concrete highways, and should adopt a value or a life-cycle assessment-based procurement process for all infrastructure and construction projects. This policy framework should be based on life-cycle analysis that would enable consideration of up-front construction costs, long term maintenance costs, environmental impacts and societal benefits and costs over the life-span of infrastructure projects.

Recommendation #2: In designing GHG regulations, the government should align Canada’s trade and climate change efforts with the U.S on such issues as price signals (timing and size); alignment on mid and long term climate objectives and avoiding disruption of cross-border trade and border adjustments due to perceived differences in approach to GHG mitigation. As well, the Government of Canada should work more productively and publicly with the Provinces and industry stakeholders towards a truly national GHG management system, and apply a sector-specific approach for designing our system which is consistent with international lessons and approaches. The government should further explore mechanisms that may be employed to guarantee Canadian manufacturers a level playing field with respect to a carbon price signal.

Recommendation #3: Make the two-year straight-line depreciation for investments in manufacturing and processing machinery and equipment permanent and enable companies to carry back any tax losses incurred as a result of this enhanced Capital Cost Allowance for a period of seven years.

Budget 2011 maintained significant investments in infrastructure and measures which succeeded in helping the Canadian economy through the recession. The cement sector recognizes and appreciates the efforts of this government to move the economy in the right direction. Cement manufacturing remains significantly challenged with continuing reduced demand from the U.S. and competition from Asian imports.

The eight member companies of the Cement Association of Canada operate 1 white and 14 grey cement manufacturing facilities in five provinces and produce over 98 per cent of the cement consumed in Canada. The industry employs over 24,000 Canadians in the production of cement, ready mix concrete and concrete construction materials, down from its 2007 peak of over 27,000 people. During 2010, member companies produced just over 12.4 mllion tonnes of cement, worth in excess of $1.4 billion. With supplementary cementing materials included, the industry’s total cement production is over 12.1 million tonnes. When both cement and concrete product sales are factored together, the industry was responsible for more than $8.1 billion in sales.

Canadian cement producers are important members of a global industry and participate in a highly-integrated North American marketplace for cement and cement products. In 2009, Canadian cement manufacturers exported more than 3.4 million tonnes of cement and clinker to the U.S., approximately one third of Canadian production. However, with the stringent U.S. regulatory environment in the context of expanding U.S. consumption, the possibility exists that the U.S. will again begin to meet demand with expanded levels of offshore, imported cement. The potential for this structural shift may affect Canadian cement exports.

Recommendation 1: Sustainable Infrastructure Investments

The debt ceiling crisis in the U.S., the subsequent crisis in market confidence has led some politicians and economists to call for Canada to return to additional stimulus to fight a possible return to recession. We do not think a return to stimulus is appropriate. But we must make a distinction between stimulus and infrastructure investments. The traditional and necessary role for federal government to support of infrastructure investments must continue and grow. The recent troubles in Montreal over the maintenance of infrastructure are a timely example of the necessity to build and maintain sustainable infrastructure.

Many, including the Federation of Canadian Municipalities, have called for a national infrastructure strategy. However, we are advocating for a new and comprehensive approach from the federal government to ensure infrastructure investments are truly sustainable. Numerous municipalities, provinces and federal policies now incorporate "green" procurement or policies for new or renovated buildings. These approaches should be increasingly integrated and sophisticated with up-to-date sustainability concepts. As well, we feel that the infrastructure debate has largely been focused on how fast money is spent, but we urge that the government play more of a roll in how well it is spent too. The motto should never be “lowest cost wins”, the motto should be “build it once, build it right, build it to last”. In this way, we will be ensuring that new projects contribute to achieving Canada’s sustainable development objectives.

Cement is the critical ingredient required for making concrete. Concrete is an essential product for virtually all construction projects, regardless of application or scale. Concrete is second only to water as the most used consumer good in the world. Concrete is also an essential enabling product for sustainable construction - when using a life-cycle approach to assess the social, economic and environmental usage impacts, concrete products present a clear advantage in many applications. Regardless of whether one is considering transportation infrastructure, small or large scale green energy projects, residential housing or large commercial industrial or institutional buildings, concrete systems provide the versatility to design and the most energy efficient, durable and cost-effective solutions.

Modern and well maintained physical infrastructure is the key to a competitive economy and healthy communities. Regardless of size, cities and communities look to modern roads and public transit, efficient water and sewage treatment facilities, proper drainage and runoff infrastructure, and energy efficient buildings and homes as the basic building blocks of prosperity and quality of life for citizens.

The CAC and Canada’s cement producers wish to be full partners with all levels of government in the development of Canada’s infrastructure. Our products provide Canada’s communities with economic benefits, social benefits and environmental benefits when compared to many of the alternatives. The CAC commends the Government of Canada for investing billions in infrastructure over the past several years and committing funds in coming years. However, Canada’s physical infrastructure still faces many challenges and a significant reinvestment in community infrastructure is urgently required.

But if infrastructure investments are important, or are in fact critical, governments must do everything that they can to ensure that we maximize these investments. In these challenging times we cannot afford to waste time or money on inefficient infrastructure investments which are avoidable. And that means that we must examine how these investments are made – both the financial and environmental costs must be examined over the full lifespan of the infrastructure.

Infrastructure investments, whether using federal funds alone or matched by other jurisdictions, should also be accompanied by program guidelines that ensure all new projects contribute to achieving Canada’s sustainable development objectives. These objectives include enhancing energy efficiency, reducing GHG emissions, reducing urban air pollution, ensuring clean water is available to all communities, managing waste efficiently and ensuring safe and efficient mobility for citizens and trade. This is particularly important for the transportation sector which is responsible for a significant share of GHG emissions.

There exists an easy opportunity for the government to adopt one of our industry’s solutions – the CSA approved and National Building Code referenced Portland Limestone Cement. We believe that the Federal Government should mandate the use of this new and equivalent cement as a substitute for of general use cement and in so doing the Federal Government can reduce up to 10% of GHG related emissions in the projects it undertakes.

Canada is a vast and expansive country requiring an extensive network of roads and highways to connect our communities and facilitate commerce. Canadians depend on safe, efficient highways to move people and transport goods to destinations within Canada and to our largest trading partner, the United States. Over the past two decades, our National Highway System has deteriorated due to inadequate public funding.

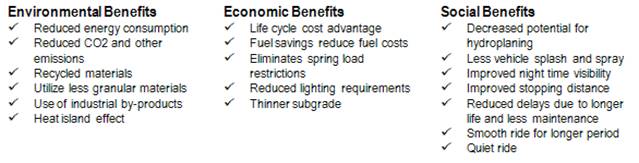

Further, the transportation sector is the largest contributor of GHG emissions in Canada, with a majority originating from road transportation. Appropriately applied, concrete pavements offer the opportunity for investment in durable, sustainable infrastructure while also achieving the additional objective of enhancing sustainability. Consider that concrete highways provide the following benefits:

Concrete highways represent a sustainable infrastructure solution to the transportation emissions policy debate. Concrete highways are cost-effective and environmentally responsible.

In order to obtain best return on investment and achieve the additional objective of enhancing sustainability through infrastructure investment, the federal government must develop policy that integrates technical, economic, environmental and social factors into decision making. The CAC therefore respectfully submits the following recommendation regarding sustainable infrastructure:

Recommendation #1: The government should make improvements in the long-term benefits of infrastructure investments by ensuring sustainability concepts are included in project design, such as the choice of concrete highways, and should adopt a value or a life-cycle assessment-based procurement process for all infrastructure and construction projects. This policy framework should be based on life cycle analysis that would enable consideration of up-front construction costs, long term maintenance costs, environmental impacts and societal benefits and costs over the life-span of infrastructure projects.

Recommendation 2: Climate Change Regulatory Policy

The Cement Association of Canada supports efforts by governments to address global climate change through the reduction of greenhouse gas (GHG) emissions and strongly believes that this can only be achieved through the adoption of regulations and policies that sustain strong and competitive Canadian and North American economies. The viability and competitiveness of our cement manufacturers depend on getting climate and air quality policy right.

The Cement Association of Canada endorses the World Business Council on Sustainable Development’s Cement Sustainability Initiative (“WBCSD CSI”) and is working aggressively to implement its four-part strategic response to climate change:

· Improving energy efficiency;

· Increase use of supplementary cementing materials;

· Energy substitution to low -carbon fuel alternative & renewable energies; and

· Research on lower GHG emitting manufacturing processes and materials.

Cement manufacturing is a highly energy intensive industry which is heavily reliant on carbon intensive fossil fuels, primarily coal and petroleum coke, making climate change policy the biggest challenge currently faced by the industry. The sector is also highly trade exposed, which combined with our energy requirements results in our unfortunately being uniquely exposed to the risks of inappropriate or poorly designed climate policies. Our sector has very limited opportunity to pass on the cost of climate change compliance to customers domestically, and has absolutely no ability to pass on costs in our primary export markets in the United States.

In promoting the transition to a lower carbon industry, policy makers must pay careful consideration to competitiveness factors and ensure that leakage of cement production and associated GHGs to less regulated jurisdictions is avoided, at all costs. Failure to do so will lead to increased GHG global emissions arising from the (unregulated) transoceanic shipment of cement products.

As the Government of Canada and the Provinces continue to develop their climate change policies, it is important that they initiate a sectoral approach in order to send a signal that governments understand the particular circumstances of the Canadian cement manufacturing sector as an energy-intensive and trade-exposed sector, and one which is completely integrated with the cement manufacturing sector in the United States of America. Anything less will undermine the competitive position of an industry that makes an important contribution to the Canadian economy and that provides Canada with a secure, strategic supply of cement that is fundamental to the expansion and greening of Canada’s infrastructure.

In the context of the potential 2012 implementation of a sub-national cap-and-trade program as announced by some of the Canadian partners to the Western Climate Initiative, we encourage the federal government to examine potential measures it could implement to assist Canadian jurisdictions in establishing a level playing field. As proposed, a cap-and-trade program would not be North America-wide, and Canadian cement manufacturers would likely be disadvantaged in both domestic and export markets, having to compete with production in non-WCI partner states as well as imports from Asian nations.

The federal and provincial governments have embarked on an ambitious process to address air quality management across jurisdictions. This process, with engagement from industrial sectors, governments and other interested parties has been successful, and we encourage the federal government to remain engaged. However, sound economic analysis, a firm understanding of firm’s stranded capital concerns, along with appropriate timelines for implementation and compliance are critical if the system is to be successful and address competitiveness concerns of industry.

Recommendation #2: In designing GHG regulations, the government should align Canada’s trade and climate change efforts with the U.S on such issues as price signals (timing and size); alignment on mid and long term climate objectives and avoiding disruption of cross-border trade and border adjustments due to perceived differences in approach to GHG mitigation. As well, the Government of Canada should work more productively and publicly with the Provinces and industry stakeholders towards a truly national GHG management system, and apply a sector-specific approach for designing our system which is consistent with international lessons and approaches. The government should further explore mechanisms that may be employed to guarantee Canadian manufacturers a level playing field with respect to a carbon price signal.

Recommendation 3: Accelerated Capital Cost Allowance

Capital investment has been and remains one of the most critical issues for manufacturers. The recent recession has had a severe impact on available capital for necessary investment to maintain or advance productivity and to become more energy efficient and reduce emissions. The recent recession has seen the largest declines in Canadian and U.S. cement consumption since the Great Depression. 2007-2009 cement consumption reported a 19 per cent decline. Cement demand advanced 10.2 per cent to just over 8.9 million metric tonnes (mmt) last year largely supported by residential construction, stimulus funded infrastructure spending, and private energy sector investment and infrastructure. This level is still more than 600,000 mt off peak levels observed in 2007. Our summer forecast suggests cement demand will decline 2 per cent this year reflecting current market performance and reduced expectations in the second half of the year, largely the result of continued uncertainty in the U.S.

The cement sector continues to believe that the government should introduce additional tax credits for manufacturers making investments in environmental technologies and processes. Budgets 2007 through 2010 introduced and extended measures that allow manufacturing and processing businesses to write off their capital investments in machinery and equipment using a two-year 50-per-cent straight-line CCA rate for eligible assets. In the 2011 budget, the federal government amended ACCA provisions aimed at allowing businesses to write business manufacturing and processing machinery investments off over three calendar years. To date, opportunities to make strategic adjustments to Canada’s fiscal regime, such as accelerated capital cost allowance, remain underutilized and must be further explored. The two-year timeframe of the accelerated capital cost allowance provided a marginal opportunity for Canada’s cement industry to realize its intended benefits due to time required to plan, obtain financing and implement new investment decisions. The further extensions provided in Budget 2011 were welcome, but still remain insufficient to properly incent needed investments. These programs also need to be expanded to recognize and include accelerated CCA for a greater number of cleaner energy use and emissions reduction related machinery and equipment.

Recommendation #3: Make the two-year straight-line depreciation for investments in manufacturing and processing machinery and equipment permanent and enable companies to carry back any tax losses incurred as a result of this enhanced Capital Cost Allowance for a period of seven years.